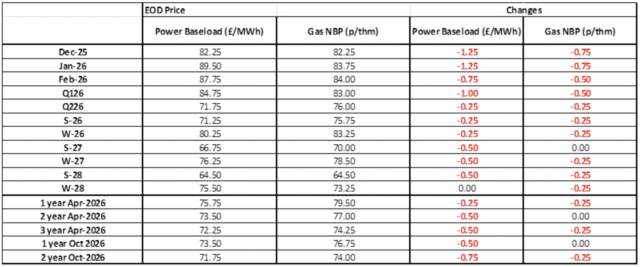

Wholesale Gas and Electricity prices eased back further on Thursday and have now both given up all of the gains seen earlier in the week.

We are seeing stability at a retail level, albeit suppliers are getting stricter on credit requirements and, therefore, factoring in larger credit risk premiums on an ad-hoc basis.

This, coupled with the increases in non-commodity costs, means that some customers are seeing increases.

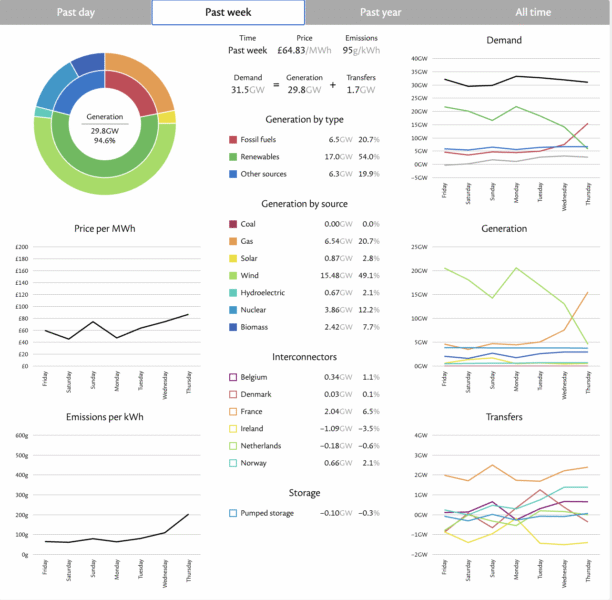

On the Generation front, electricity was below £65/MWh which is encouraging for this time of year and indicative of 54% of production coming from renewables of which the bulk, as you would expect, was from wind. Fossil fuels were just 21% of Generation source last week.

We expect the Generation price to rise as we go into winter and fossil fuels become more dominant as temperatures drop.

#gas #electricity #businessutilities #businessgas #businesselectricity