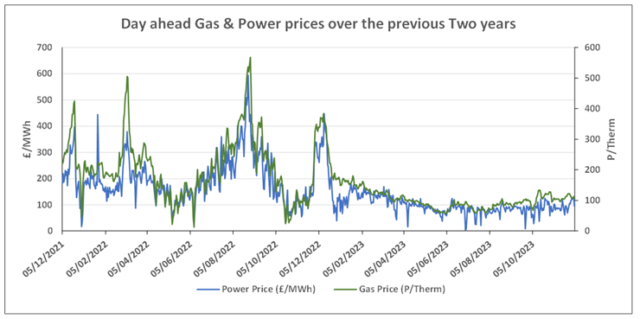

As anticipated wholesale gas & electricity prices dropped again yesterday; finally we hope that the traders have backed off and market fundamentals are kicking in as stocks are high and future supplies presently unobstructed.

Since COVID & then Ukraine, normal market conditions have not existed and this is a further example of that with significant reductions in the winter. It was previously unheard of to see lower gas & electricity prices in December than May/June.

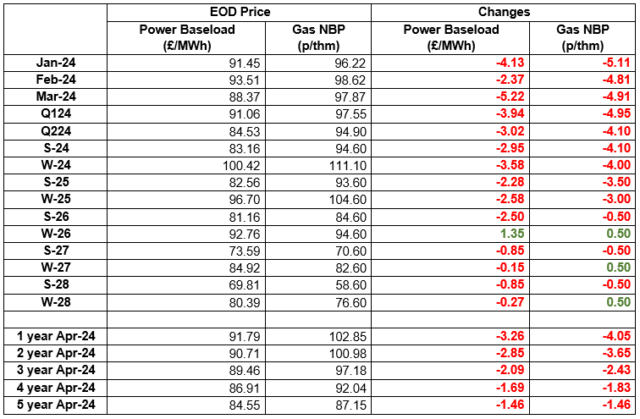

| Gas: NBP contracts continued to fall yesterday. Strong European stock levels limited British export demand whilst British LNG nominations are set to rise 10%, adding pressure to prompt contracts. Average Norwegian flows to Britain from the Langeled pipeline are expected to reach 98% of the pipeline’s daily capacity. Power: Lower than expected wind output boosted the day ahead price yesterday, although all other contracts fell in value – once again tracking NBP hub losses. Next week, wind output has been revised upwards whilst rising temperatures are likely to limit any heating demand. Oil: Prices proved volatile yesterday as the market weighed up production cuts and global demand. Come January voluntary cuts will reach 2.2m bbl/day. Carbon (EU ETS): The ICE Dec-23 closed at €68.64 yesterday. Opening at €69.10/t this morning, the contract has been volatile but is currently trading down at €68.85/t at the time of writing. Carbon (UKAs): The ICE Dec-23 fell to £35.33/t during yesterday’s session. The contract is currently trading at £35.59/t |