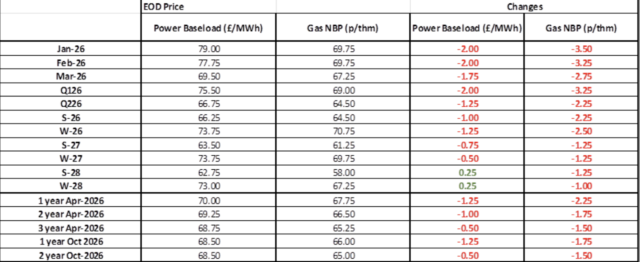

On Thursday wholesale Gas and Electricity prices continued to drop to extend their 10-day run.

While the actual wholesale prices are very favourable, these tend to be more than outweighed by increases to non-commodity charges, most of which are levies from the Government.

On the retail front we are seeing prices creeping up, which is unwelcome, although the increases are clearly contained because of the reduction in the actual commodity price at wholesale level.

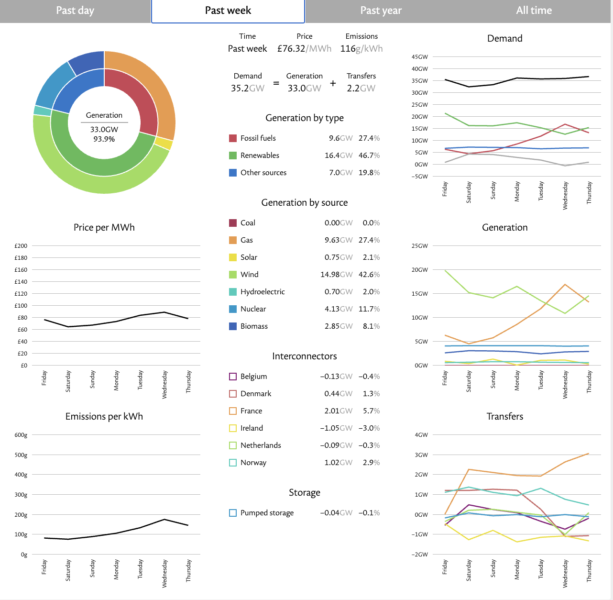

On the electricity generation front prices dropped back slightly last week to £76.32/MWh, driven by renewables being at 47% with fossil fuels being at 27%.

| Gas: Gas prices continued to fall yesterday. Continued mild temperatures, alongside a return to average wind generation and ample supplies of LNG, has softened prices in the prompt. Curve prices are continuing the downtrend set by the prompt with the LNG market removing the risk premiums out of the curve prices. Power: Power prices tracked the Gas market yesterday and continued to fall. In the prompt, wind generation has returned to norms, with the expectation of being 20% above norms during week 50 (next week) limiting demand for fuel-fired generation. Oil: Oil prices rose yesterday. Investors’ expectations of the Federal Reserve to cut interest rates and spark new demand, whilst stalled Ukraine and Russian peace talks limited the likelihood of restoring Russian flows into the market. Carbon (UKAs): The ICE Dec-25 rose to £56.83/t yesterday. The contract has not started trading at the time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity