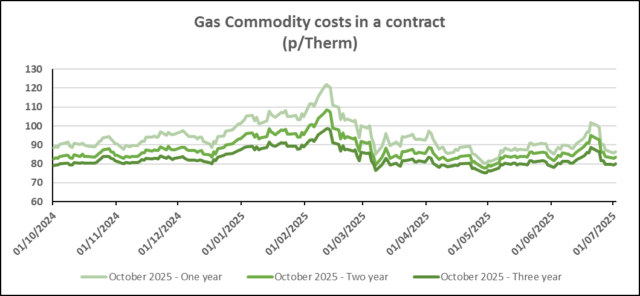

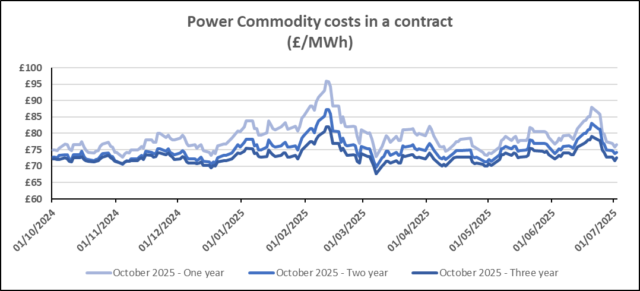

Wholesale gas and electricity prices were broadly stable on Thursday, with the electricity price still below £80 per MWh. The spread has increased over the last few days, and with three-year prices almost 10% below one-year prices, the indicators clearly suggest that the market has further to drop.

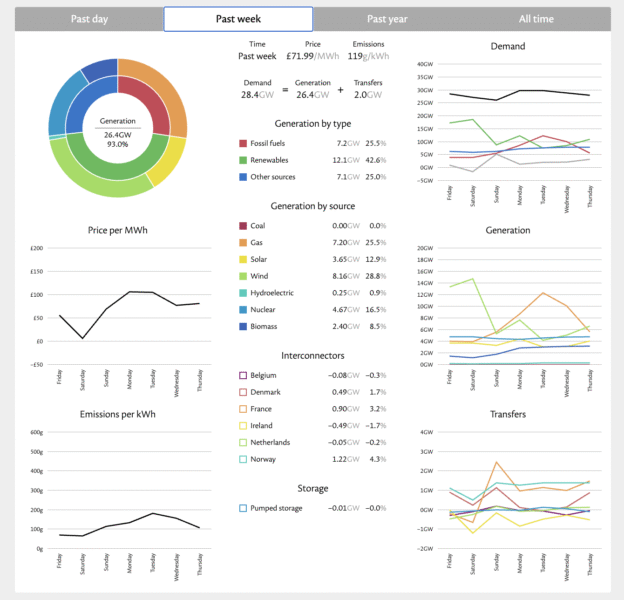

On the generation front, prices ticked up to over £70 per MWh in the past week as the percentage of production from fossil fuels increased from 20% to 25%. Whilst it’s been very sunny, the main source of renewable energy is wind, which is why there has been more fossil fuel production.

It was interesting to see in the media this week that the government is threatening to spend tens of billions to get the infrastructure sorted so that, when renewable energy is produced, it can actually make it into the grid. This is because, at present, there are bottlenecks, and often renewable production does not make it into the grid and is totally wasted.

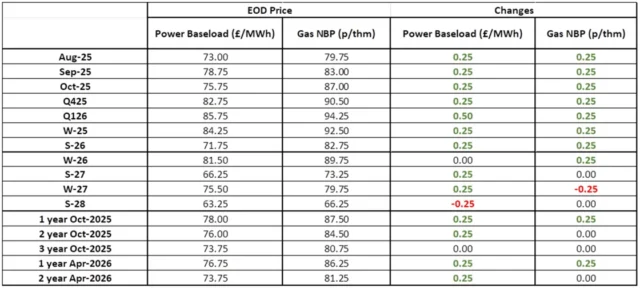

Gas: NBP contracts settled slightly higher yesterday. Prompt prices were supported by a reduction in wind output for week 28. Early morning gains in the front month were reciprocated throughout the far curve.

Power: There were modest gains throughout the curve yesterday with temperatures well above the seasonal average. Gains in benchmark UKA prices and NBP movement supported the Winter 25 contract and beyond.

Oil: Crude front month prices gained yesterday despite fears over what may happen with US tariffs when the current hold period ends on 9 July. OPEC+ are also expected to raise production by 411,000 bpd.

Carbon (EU ETS): The ICE Dec-25 rose to €72.06/t yesterday. Opening at €72.21/t this morning, the contract is currently trading at €71.87/t.

Carbon (UKAs): The ICE Dec-25 rose to £48.50/t yesterday. The contract opened at £48.08/t and is currently trading at £48.15/t.

#gas #electricity #businessutilities #businessgas #businesselectricity