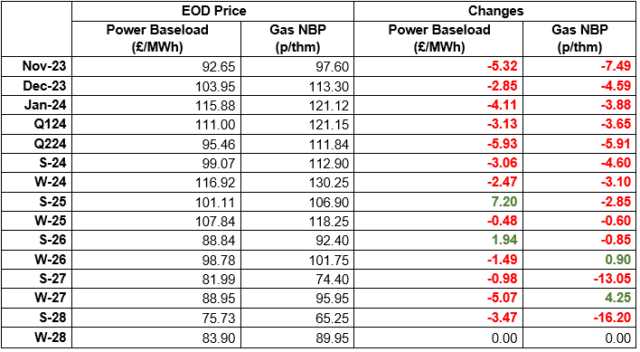

Prices continued to drop with the exception of S25, which rose markedly, and S26 which rose less so.

Q2 24 & S24 are both now below the psychological £100/MWh, while pressure on near term prices supports our strategy of contracting for winter in the next 10 days max. while the weather remains warm and these prices are dropping.

Gas: Gas prices fell yesterday. British demand totalled at 161MCM, 80MCM below seasonal average, and the grid being 12MCM long yesterday. Norwegian supplies into Easington rose by 53%.

Power: Power prices continue to be swayed by the Gas market yesterday. Additionally, UK wind generation is forecast to operate 20% above seasonal norms throughout this week. UK Wind Generation output an average 7.3GWs throughout September, 0.6GWs more than the 2018-2022 average.

Crude: Oil continued proving to be volatile yesterday, with its morning gains being pushed by the market awaiting a decision on interest rates in the US. Prices continue to rise with support from the supply cuts from OPEC+ members Russia and Saudi Arabia.

Carbon (EU ETS): The ICE Dec-23 closed downwards at €80.8/t yesterday. The market opened this morning at €80.63/t and is trading at €80.47/t at the time of writing.

Carbon (UKAs): The ICE Dec-23 closed flat at £39.64/t yesterday. The contract is currently trading at £39.35/t at the time of writing.