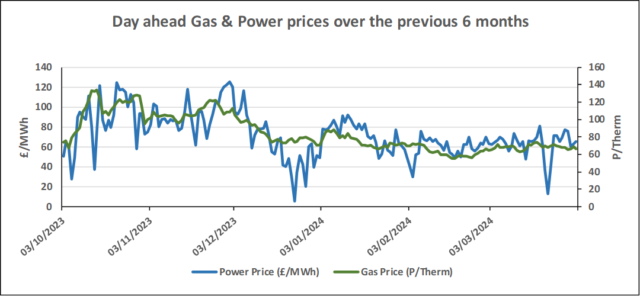

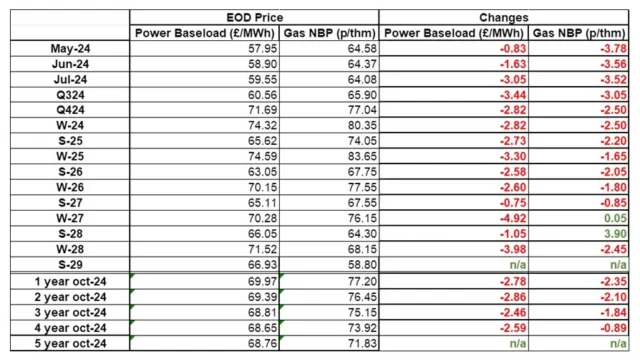

Wholesale Gas and Electricity prices continued their drops on Tuesday, and have almost completely wiped out two weeks’ worth of gains in three days.

As previously stated, we expect this trend to continue as the market fundamentals remain strongly against pricing increases.

| Gas: Forecasts of increased wind generation over the next fortnight helped pressure NBP contracts yesterday. British demand was below seasonal average yesterday, placing further constraint on the prompt. This morning, during early trading, prices have eased off further against last night’s close. Power: Near curve contracts shed value yesterday. This was largely due to increased forecasts for wind output, and the return of nuclear generation at Heysham reactor 1 and Hartlepool reactor 2, following outages. Further out on the curve, prices fell in line with the wider energy complex, namely NBP and carbon. Oil: Oil markets were bullish yesterday. Benchmark Brent contracts exceeded $89/bbl for the first time since October. Ongoing attacks by Ukraine and Russia on each other’s energy infrastructures are increasing supply concerns in the market. Manufacturing activity increases in China have boosted demand expectations. Carbon (EU ETS): The ICE Dec-24 closed at €58.72 last night, down on last week’s closing price. Opening higher this morning the contract is currently trading down at €58.50/t. Carbon (UKAs): The ICE Dec-24 closed at £34.93/t yesterday. At time of writing today, the contract is yet to trade. |

#gas #electricity #businessutilities #businessgas #businesselectricity