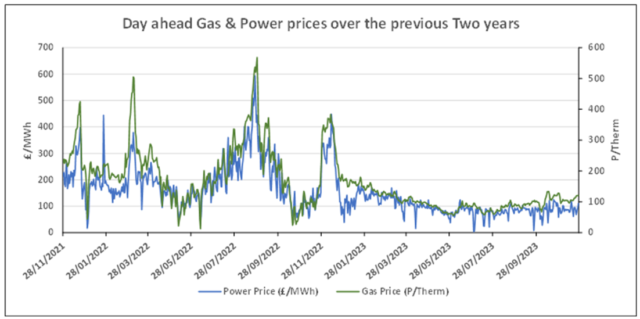

Wholesale prices continued to drop on Wednesday as the market fundamentals of good stock and plentiful supply dominate.

Future wholesale prices are now below their previous low point at the end of May/early June.

| Gas: NBP contracts continued to fall in price as the market proved fundamentally bearish. Day ahead contracts were pressured from LNG send out, however losses were capped by below average wind generation. Power: Power contracts, once again, tracked their NBP counterparts yesterday, whilst further pressure was applied due to the falling carbon market. (For todays price outlook, as of last nights close, please see the table below) Oil – Oil prices proved volatile throughout yesterday’s session as the market awaited the latest OPEC+ supply agreement which has been delayed since 26th November so far. Output from Kazakhstan oil fields has been reduced, it is likely that this reduction will continue into December. Carbon (EU ETS): The ICE Dec-23 traded down to €71.02 /t yesterday. This morning the contract has opened steadily , at time of writing it is trading at €71.10/t. Carbon (UKAs): The ICE Dec-23 fell to £41.58/t during yesterday’s session. At time of writing the contract is trading at £41.79. |