On Monday, wholesale Gas and Electricity prices continued to drop which is welcome news and very unusual for this time of year.

In addition, the curve is opening up slightly, albeit longer term contracts are still cheaper than short term.

For once the pricing is being driven by ‘typical’ factors, this time milder than expected weather.

Unfortunately, as we have repeatedly said, any benefit from lower unit rates is balanced out by increases on the non-commodity costs.

Gas: Prices continue to fall as forecasts of mild weather persist. Worries about supply for winter are starting to reduce on the back of weaker than expected demand.

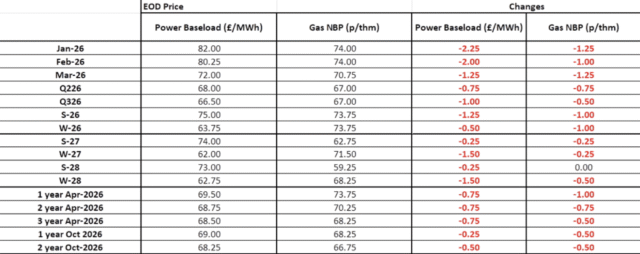

Power: Power prices dropped in value yesterday, influenced by weakening NBP prices. Weather fundamentals helped drive prompt prices down. For a price outlook, as of last night’s close, please see the table at the bottom of this update.

Oil: Prices gained yesterday. Geopolitics were at the forefront with drone attacks on oil infrastructure in the Black Sea. The market remained cautious, however, as concerns of oversupply in 2026 persist.

Carbon (EU ETS): The ICE Dec-25 fell to €82.64/t by close yesterday. The contract opened today at €82.42/t.

Carbon (UKAs): The ICE Dec-25 finished trading at £56.46/t yesterday. Opening this morning at £56.72/t.

#gas #electricity #businessutilities #businessgas #businesselectricity