Wholesale gas and electricity prices continued to rise on Wednesday, for the third day in a row.

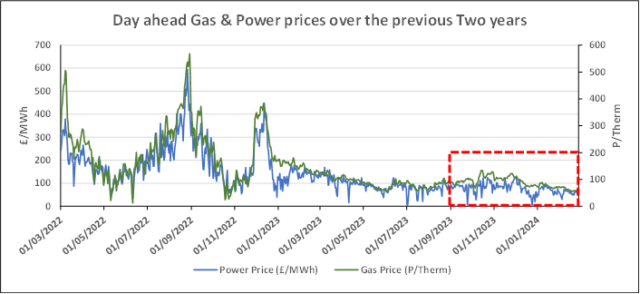

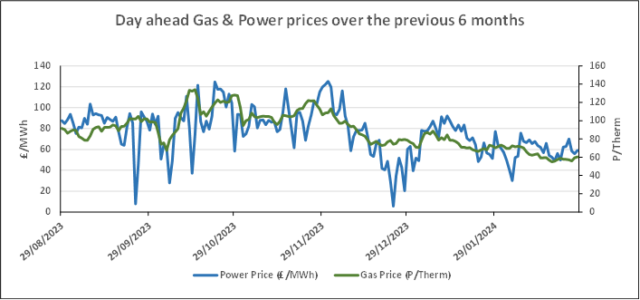

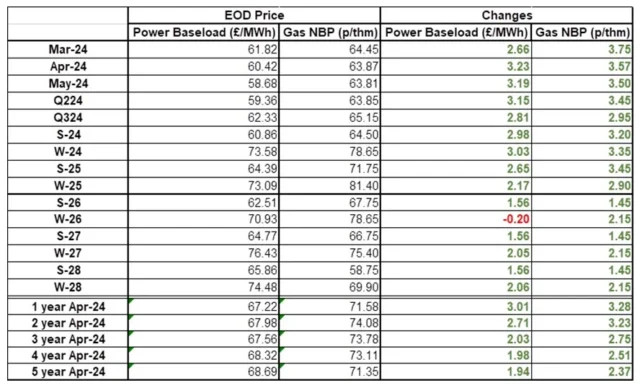

That said, Winter 24 Gas remains below 80p/thm and apart from Winter 24 and Winter 25 the curve is pretty flat going forward.

Our view remains that anyone entering into gas and electricity contracts should only commit to a maximum of one year out, despite what other brokers may be advising.

The fundamentals of strong supply, increasing gas deduction and good local stocks will force pricing down.

| Gas: Prices gained yesterday following the culmination of the T-4 capacity auction, with gas fired generation being the main source of existing capacity units, with an awarded capacity total of 28.2GW. Outages at the Barrow gas treatment plant is expected to end today, after another extension. Power: Contrary to bearish fundamentals, yesterday’s power prices continued to rise. Wind generation has been revised upwards for next week, bringing output close to seasonal expectations. 3 LNG cargo are expected on British shores between 1-10 March, during this period last year there were 13 vessels. Oil: Despite news from the US that there will be no interest rate cuts coming soon, the market remains well positioned by the prospect of OPEC+ continuing its 2.2m bbl/day cuts. At present crude prices have seen gains for 5 weeks in a row. Carbon (EU ETS): The ICE Dec-24 closed at a week-long high of €57.84/t yesterday. After a busy morning’s trading, the contract is currently at €57.71. Carbon (UKAs): The ICE Dec-24 gained again yesterday, closing at £37.00/t. The contract is currently trading, slightly down, at £36.90/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity