After my prophetic words of wisdom earlier the market dropped markedly yesterday due to strong wind outputs which are expected to remain above seasonal averages throughout the next week.

My view for the long term remains as it was earlier and is that gas prices will stay where they are/increase. We have more control locally over electricity with increasing wind power coming on stream.

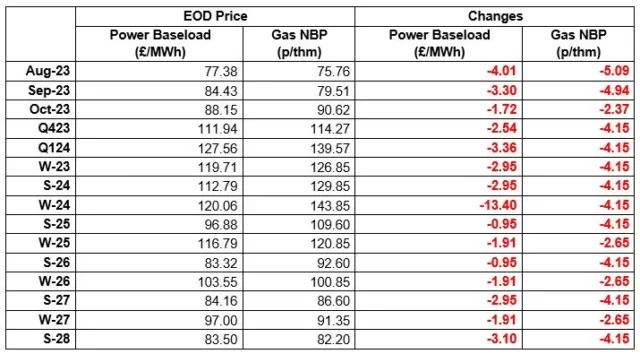

Electricity for W23, W24 & W25 is in a very flat price range from 116.79 (W25) to 120.06 (W24) with W23 at 119.71 which would lead us to suggest considering 24M contracts even though the summer curve is in a broader range over the same period.

| Gas. NBP contracts fell throughout the curve yesterday. Wind output forecasts nearly doubled day on day yesterday and are predicted to remain well above seasonal average throughout next week. Power: Power contracts tracked NBP losses yesterday. Wind forecasts are expected to be around 20% above average throughout the coming week which is helping to keep prices bearish. (For today’s price outlook as of last nights close, please see the chart below). Crude: Oil prices dropped yesterday as US interest rates reached a 22 year high. Potential prolonged Saudi production cuts added further bearish sentiment. Carbon (EU ETS): The ICE Dec-23 contract dropped to €90.84/t yesterday. Opening lower at €90.62/t today, it has since fallen to €89.65/t at the time of writing. Carbon (UKAs): The ICE Dec-23 contract seen losses yesterday, closing at £47.53/t. Today the contract opened at £48/t and has since fallen to £47.51/t |