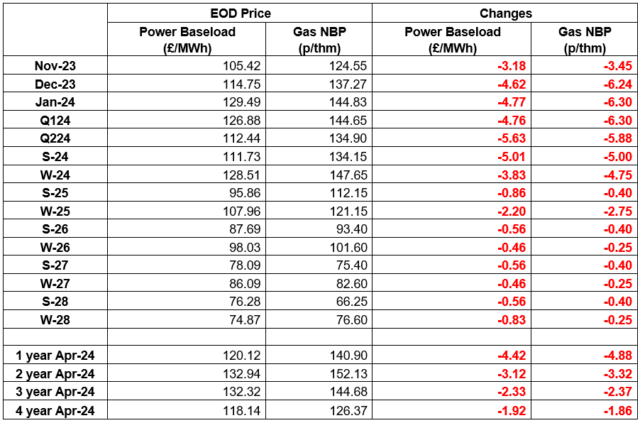

Wholesale prices continued to drop back on Wednesday with the largest drops seen on Dec 23 through Q1 24 which is good news.

The drops are driven by more LNG cargoes due to arrive, high local stocks of LNG and warmer than expected forecasted temperatures despite lower than anticipated wind generation

Given that retail prices didn’t take 100% of the wholesale increases, the drops are coming through but not on a like for like % basis

Gas: Gas prices fell across the curve yesterday as Europe is predicted warmer weather than initially forecasted. However, Gas demand continues to rise as the seasonal weather becomes colder. Storage sites saw a net withdrawal yesterday.

Power: Power prices continued to be influenced by movements in the wider energy complex. UK Wind generation is predicted to output 6.2GWs/day, 2.6GWs below seasonal average.

Crude: Oil prices were volatile yesterday as the scene in the Middle East continues to influence prices. Prices saw gains as supply concerns grew. However, the $USD strengthened against multiple currencies not seen since the beginning of October, providing bearish influence on prices.

Carbon (EU ETS): The ICE Dec-23 fell to €79.92/t yesterday. The contract is currently trading at €79.72/t at the time of writing.

Carbon (UKAs): The ICE Dec-23 fell to £39.14/t yesterday. The contract is currently trading at £38.5/t at the time of writing.