26th July 2023 Energy Price Alert – UK Gas & UK Electricity

The market continued to rise on Tuesday and our view as of now is that this will continue. There may be odd daily drops but gas retail prices have risen 10% since the low point of early June. A recent Bloomberg report showed the highest volume of LNG sitting in ships not going anywhere which means that traders are manipulating the market up waiting for the right price before striking for the delivery point. This is driven by the facts that i) European gas stocks are at a high for this time of year and ii) Chinese demand is coming back strongly. Qatar and the USA each produce 40% of the world’s LNG with Australia producing around 12%. We can take cargoes from both the USA and Qatar, Australia is not viable for Europe presently. USA LNG is expensive because it is produced by fracking.

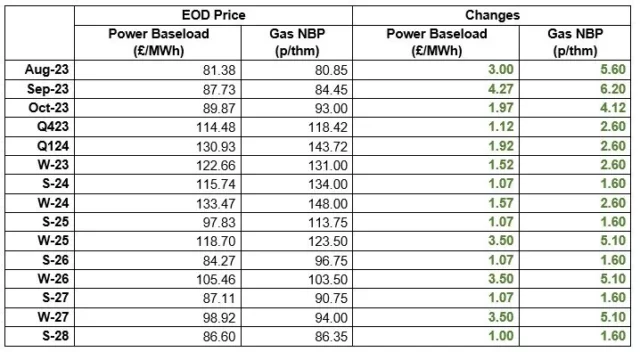

Our advice therefore has changed and we are recommending fixing contracts. How far in advance of your current contract expiry you choose to fix is for discussion because you can see from the table below that near term prices drop markedly from the forecast rates. It’s a certainty vs risk discussion.

Our recommendation, based on the curves in the table below, is to fix for a minimum of 12 months. Our further recommendation is to take advantage of supplier flexibility to ensure that expiry is not between 1/11 and 31/3, ideally 1 month extra each side, in order to avoid renewing when prices have historically been high.

Gas: NBP contracts seen further gains yesterday. Lack of LNG landing on UK shores was perhaps a driver of near curve prices, with the market likely lifted to attract LNG cargo. Market fundamentals helped support the position. This morning has seen further increases in near term contracts.

Power: Power contracts seen bullish sentiment yesterday as their NBP counterparts seen gains throughout. Carbon prices once again supported far curve movements. Wind output has been revised upwards over the coming weeks. For todays price outlook, as of close last night, please see chart below

Crude: Oil prices gained throughout yesterdays session supported by a weakened US dollar making. Several sources are also speculating interest rate cuts early into next year which is helping to support price.

Carbon (EU ETS): The ICE Dec-23 contract rose to €91.93/t yesterday. Opening higher at €92.28/t today, it has since risen to €93.19/t at the time of writing.

Carbon (UKAs): The ICE Dec-23 contract seen gains yesterday, closing at £47.86/t. Today the contract opened higher at £48.35/t but has since fallen to £48.24/t

×

Enter Email to Continue

Please provide your email to access the procurement resources.

Join us...

and 2000+ other CFOs and FDs who are already enjoying our free resources and industry insights.