Wholesale gas and electricity prices eased further on Monday, which was a welcome development. However, we expect continued volatility as the situation in the Middle East continues to evolve.

Prices remain higher than they were two weeks ago, so it’s reasonable to expect further downward movement in the coming days.

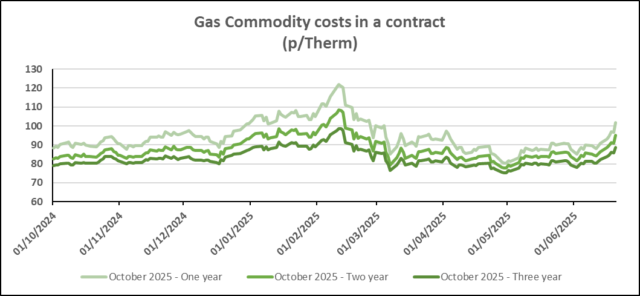

Gas: The majority of NBP contracts finished yesterday’s session down. Norwegian maintenance continues, however flows into Easington on Monday increased. High temperatures are expected to continue throughout June and July increasing cooling demand. Any lull in renewable output would potentially increase gas for power demand. Following the announcement of a ceasefire between Israel and Iran, early trading is well below last nights close, with an c.9% fall in the Winter 25 contract.

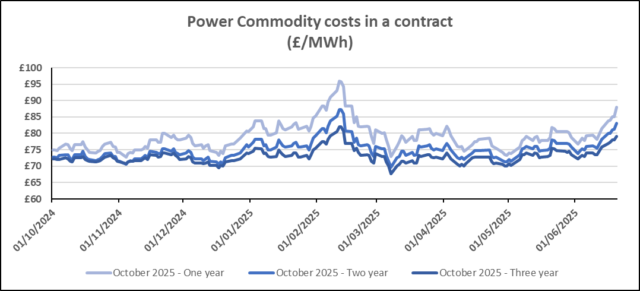

Power: Most contracts fell in value throughout the curve yesterday, with movements in NBP and carbon contracts adding pressure. Strong wind output is expected for the remainder of the week, however; solar output is expected below norm. An unplanned outage at the IFA1 interconnector with France was expected to be back up and running last night. Similar to gas, power trading has also opened lower this morning with a c.6% fall in the Winter 25 contract.

Oil: Benchmark oil contracts shed value yesterday, following Iran’s decision not to stop traffic through the Hormuz strait, instead retaliating with strikes against a US military base in Qatar. News of a ceasefire between Israel and Iran late last night has caused the market to open lower than last nights close.

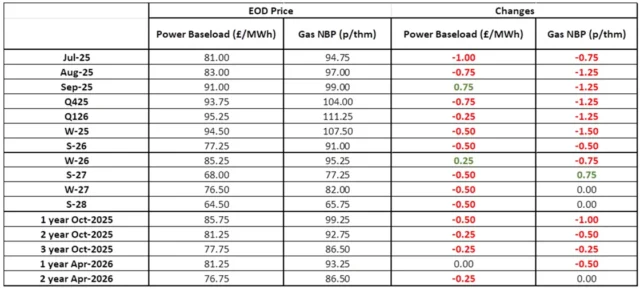

Carbon (EU ETS): The ICE Dec-25 rose to €73.27/t yesterday. Opening at €73.11/t this morning, it is currently trading at €73.50/t.

Carbon (UKAs): The ICE Dec-25 fell to £50.79/t by last nights close. The contract opened lower this but is currently trading at £51.50/t.

#gas #electricity #businessutilities #businessgas #businesselectricity