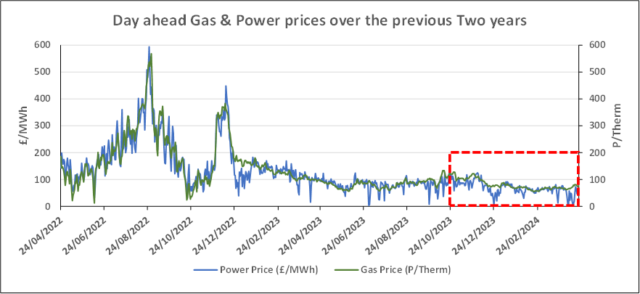

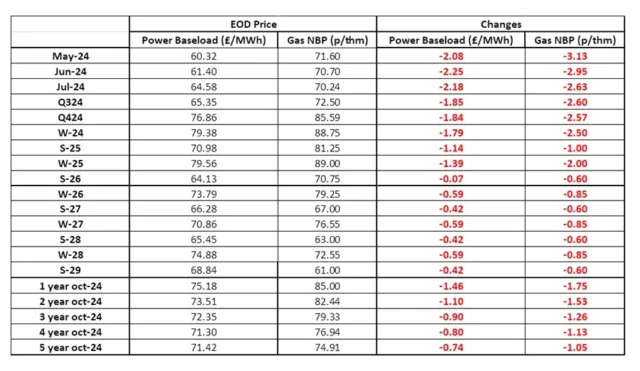

Wholesale Gas and Electricity prices continued their drops on Tuesday, with both Winter ’24 and ’25 Electricity now back below £80/MWh.

Now that the geo-political issues in the Middle East have abated, we expect to see further reductions to at least the levels seen in March.

As prices drop the curves are also flattening, although there remains a delta between 1 and 2/3 year contract pricing as a result of the recent turmoil which had a more pronounced impact on nearer term contracts.

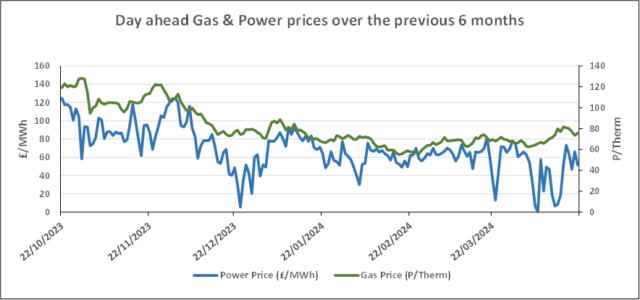

| Gas: Prices fell yesterday, backed by increased wind generation and expectations of a decline in day-on-day demand. Gas storage in the UK has reached its highest levels, for this date, in three years. Power: Near curve prices followed movement at the NBP gas hub yesterday, whilst out on the curve increases in key UKA prices helped realise slight gains on some contracts. Temperatures for the rest of the week remain below seasonal average, likely increasing heating demand. Temperatures are expected to rise as we move into next week. Oil: On the whole, oil prices rallied yesterday. It’s expected that the US will invoke sanctions on Iranian oil production, with voting expected to take place this weekend. As the US economy grows, the prospect of interest rate cuts moves forward providing, an upper limit to price movement. Carbon (EU ETS): The ICE Dec-24 fell to €65.67/t yesterday. This morning the contract is currently trading at €66.77/t. Carbon (UKAs): The ICE Dec-24 closed higher at £36.72/t yesterday. The contract opened higher this morning at £37.25/t , at time of writing it’s trading at £36.75/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity