On Thursday, wholesale gas and electricity prices rose markedly, adding to the gains of Wednesday. We are hopeful that this is a short-term blip, as there are no real market fundamentals driving it. At the retail level, we have been signing electricity contracts below 20p per kWh for daytime rates and around 15p per kWh for night, with gas in the 3.5p–3.8p per kWh range this week.

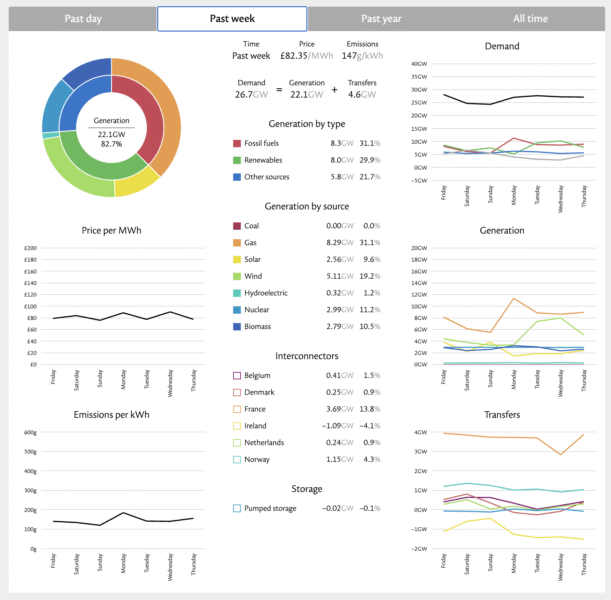

On renewals, we are finding that non-commodity costs are causing issues and offsetting some of the unit rate gains. If you would like a detailed paper on this, let us know and we will get it over to you.On the generation front, prices in the past week went over £80 per MWh, driven by fossil fuels being the dominant generation method at over 31%, while renewables fell below 30%. All in all, not a great way to start the bank holiday weekend but hopefully next week will be better!

| Gas: Gas prices rose yesterday. A lack of renewable generation in the prompt lead to an increased demand for gas fired output. A low pressure system is expected to bring rain to parts of Europe. Unseasonably cool temperatures were forecasted in Norway leading to an increase demand across other markets, driving prices higher. Power: Power prices increased yesterday. A low renewable output of 2.4GWs for wind and 3.1GWs for solar, supported the gains. The power curve continued to rise, tracking the strengthening wider energy complex. Oil: Oil prices rose by 1% yesterday as the peace negotiations between Ukraine and Russia stalled, ensuring the sanctions on Russian oil remained. U.S data showed strong demand for oil, further feeding into the prices. Carbon (EU ETS): The ICE Dec-25 rose to €72.62/t yesterday. The contract opened at €72.61/t this morning and continues to trade back at this level after €72.35/t earlier in the session. Carbon (UKAs): The ICE Dec-25 jumped up to £52.05/t yesterday. The contract opened at £52.64/t this morning and is currently trading at £52.27/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity