On Friday there was minimal movement at the wholesale level on gas, but slightly more on electricity, albeit still negligible.

Our view is that prices are now going to keep on steadily rising, with the odd downward blip.

At the macro-economic level the Chinese stimulus announced earlier today has had a mixed reception and is not seen as a major boost to their economy. With 25%/30% of their GDP coming from the housing sector, where they now face some huge bankruptcies, tough times are ahead and the risk of contagion in to their banking sector from loan defaults will cause problems for the ruling party. One would like to think that will reduce the upward pressure on LNG prices but let’s see.

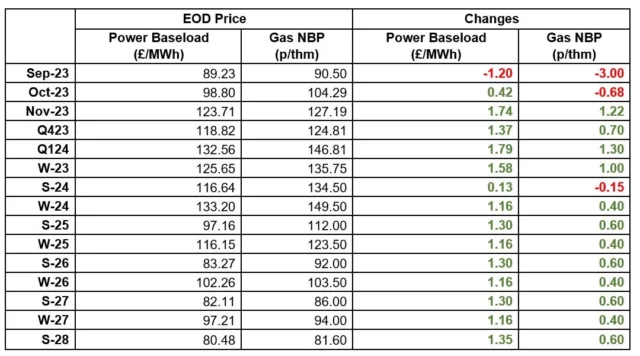

Gas: Gas prices fell in the prompt but rose across most of the further out contracts. A combination of Australian LNG strikes and upcoming Norwegian maintenance has caused prices to rise. Prompt fundamentals saw a decline in demand for gas-fired generation due to the expected rise in wind generation.

Power: Power prices were influenced by the gas market. The timing of the Australian LNG strikes would impact supplies for Winter 2023, increasing competition from consumers for LNG and raising prices.

Crude: Despite oil prices rising last Friday, market sentiment is heavily bearish this week. Poor Chinese economic data, a strengthening $USD and the US Federal Reserve not declaring their plan for interest rates look to begin to reduce the previous seven weeks of gains.

Carbon (EU ETS): The ICE Dec-23 closed at €88.01/t last Friday. Opening today at €88.24, the contract is trading at €87.2/t at the time of writing.

Carbon (UKAs): The ICE Dec-23 closed at £43.39/t last Friday. The contract has opened at £43.05/t today, and is currently trading at £43.2/t.