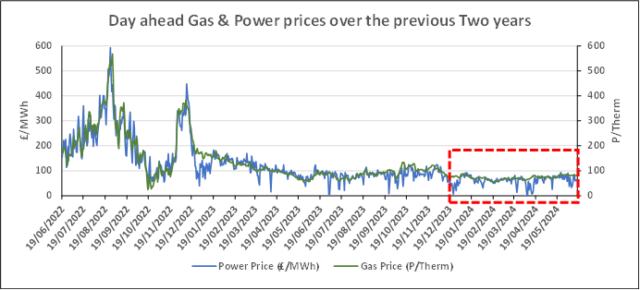

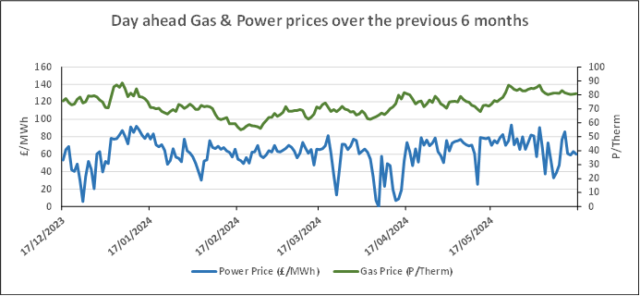

On Tuesday wholesale gas and electricity were broadly stable with small increases across the board due to a Norwegian outage.

In the past, such outages have resulted in far larger increases and we take this small movement as an indication of the supply strength in the current market.

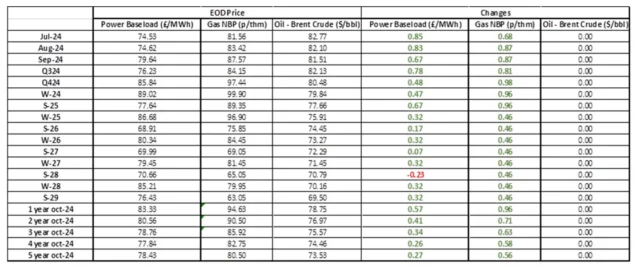

| Gas: Gas prices rose yesterday following a new outage at Norway’s Nyhamna processing plant, adding 33.8mcm/day to the ongoing 15.4mcm/day outage at Visund. The next shipment of LNG to dock in the UK is expected on 26 June, adding further supply limitations. Power: The power curve increased across most contracts yesterday. The power market continues to track the wider energy complex, with gains in UK carbon increasing the far out curve. A revised downwards projection of wind generation, combined with a full capacity outage of the 1.4GW Viking link between the UK and Denmark, pushed prices upwards in the near curve. Oil: Oil prices rose yesterday amongst hopes of a US interest rate cut in September. The Federal Reserve commented that inflation was moving in the “right direction”, leading to restored hopes among investors for increased demand. Carbon (EU ETS): The ICE Dec-24 found support yesterday, settling higher at €68.50/t. This morning, the contract has found further support and is currently trading at €68.83/t. Carbon (UKAs): The ICE Dec-24 closed upwards at £50.03/t yesterday. This morning, the contract has opened softer, trading at £49.84/t at time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity