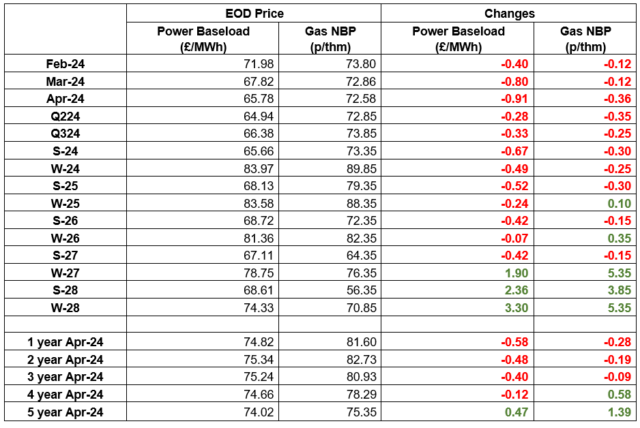

As forecast, gas and electricity prices continue to drop.

This is hugely counter cyclical as we have become accustomed to prices rising during the Winter.

The reason for the continued reductions is significant over-supply forecast to go in to the next decade.

Short-term contracts remain the best way to secure yourself against this risk on portfolios of less than 10GWh.

| Gas: Gas prices softened yesterday as bearish fundamentals weighed on most contracts. Although prompt demand is high due to the colder weather, overall supplies remain ample, and the Grid is balanced. Power: Power prices followed the Gas market yesterday. Wind generation is forecast to jump upwards to 16.5GWs/day through week 4, 6.9GWs above average output. Temperatures are currently forecast to flip from the current 1°C average to 8.5°C average over week 4, limiting heating demand. Oil: Oil prices edged upwards yesterday as rising tensions in the Middle East went against a rising $USD. More tankers are now avoiding the Suez Canal, re-routing around South Africa causing delays and increasing costs. Carbon (EU ETS): The ICE Dec-24 fell to €65.59/t yesterday after a brief gain in the previous session. Opening at €65.20/t this morning, the contract is now trading at €65.10/t. Carbon (UKAs): The ICE Dec-24 fell to £34.76/t yesterday, continuing the recent bearish run. The contract is currently trading at £34.17/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity