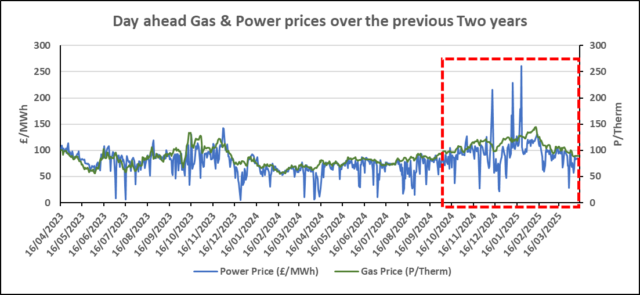

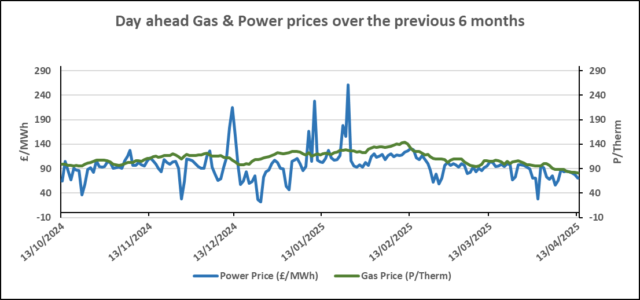

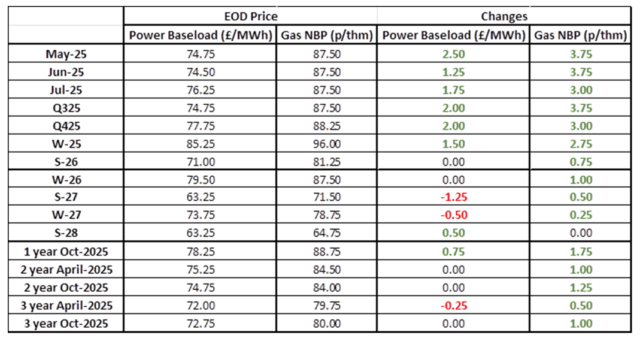

Wholesale Gas and Electricity prices continued to be a little volatile, although with baseload Electricity below £80/MWh and Gas below 90p/thm we are still seeing very competitive retail prices.

On the generation side: power last week was £77.03/MWh, with renewables being below 40%.

That said, biomass and nuclear were over 24%, so non-fossil fuel production was over 60% of the total in the past week. As the global macro-economic situations settle, we expect to see further softening of prices.

Interestingly, there was an article yesterday that said during Summer this year it is anticipated that power stations will be put on standby due to the volume of non-fossil fuel production. This is good news for the UK.

| Gas: The gas market saw gains across all contracts yesterday. In the prompt, a drop in average temperatures and a revised downwards forecast of wind generation pushed prices upwards. Curve prices also predicted a drop in renewable generation, leading to increased demand for gas. However, gains were limited as total demand is expected to fall within the summer months. Power: Power prices were bullish yesterday. A drop in wind generation saw the day ahead price rise, but further gains were limited by an above average output of 3.3GWs/day from solar sources. Oil: Oil prices rose yesterday on the hopes of potential talks between the US and China. With no further details, the market sentiment suggests any further information would be bullish. China’s economy grew by 5.4% year on year for Q1, however this figure may be inflated. Carbon (EU ETS): The ICE Dec-25 rose to €66.97/t yesterday. Opening stronger this morning at €67.25/t, the contract has fallen since and is currently trading at €66.77. Carbon (UKAs): The ICE Dec-25 settled flat yesterday at £47.40/t. The contract opened at £47.27/t this morning and continues to trade at £47.09/t at the time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity