The see-saw’ing continued with wholesale prices dropping yesterday. Wind production over the next 2 weeks is expected to be above seasonal norms and if that comes to pass it will present an opportunity to lock in electricity contracts. Gas prices should also subdue as demand is reduced but there are other global macro-economic factors at play there.

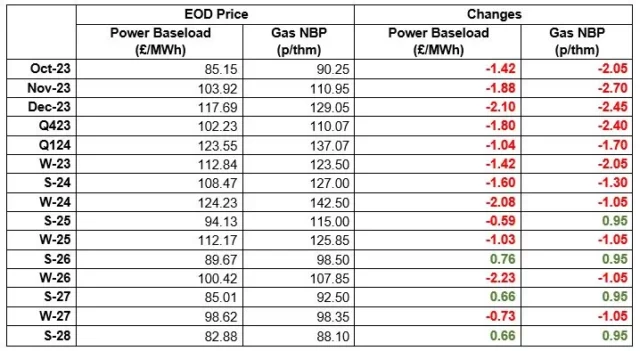

As I’ve been saying the disconnect between gas & electricity pricing is now very evident. To get that in to context prices on 5/6/23, which was a previous low point for W23, were as follows:

| Power | Power £/MWh | Gas p/thm | Power £/MWh | Gas p/thm |

| Today | Today | 5/6/23 | 5/6/23 | |

| W23 | 112.84 | 123.50 | 114.12 | 105.45 |

| W24 | 124.23 | 142.5 | 114.95 | 117.45 |

In terms of our weekly generation update in the lower table renewables were at the lowest level I’ve seen in a long time, 21.1%. That said “Other” – nuclear and biomass – were at their highest and still better for us all than fossil fuels. There were increased transfers in from abroad and the generation price at £91.65/MWh was higher than usual for this time of year.

Wishing you a lovely weekend

| Gas: Gas prices fell in value yesterday caused by strong wind output forecasts over the next two weeks. Shipping signals and port data indicate Britain should expect to see three LNG vessels docking before the end of September. This morning, the market has seen a further fall in near curve contract pricing. Power: Price volatility was seen to continue throughout yesterday’s session, with the previous day’s gains being reversed. Losses once again tracked the NBP markets. Next weeks wind generation has been revised upwards, with expected levels 20%+ above seasonal norms. Crude: Oil prices reached further highs for the year yesterday. Supply concerns were the main price driver, trumping worries over economic growth. The US dollar climbed to its highest point since early March. Carbon (EU ETS): The ICE Dec-23 closed at €83.12/t yesterday. Opening down today at €82.86/t, the contract has rallied and is trading at €83.57/t at time of writing. Carbon (UKAs): The ICE Dec-23 closed at £39.01/t yesterday. Opening at the same price this morning, the contract is currently trading at £38.68/t. |