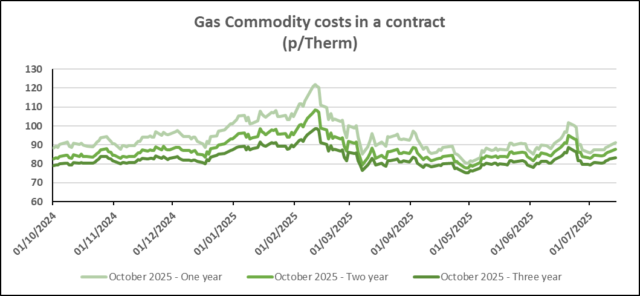

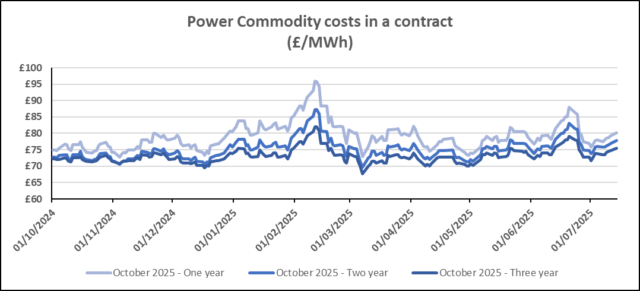

Wholesale gas and electricity prices both rose on Friday, with more sustained increases in gas than in electricity. It’s interesting to note that we are now seeing clear differentiation in the daily price movements between gas and electricity, though it’s uncertain how long this trend will continue.

Our view remains that there is still some room for the markets to drop. However, at the retail level, these wholesale movements are having minimal impact, as they are focused on the short term rather than further out. These changes will therefore primarily affect clients with flexible contracts who have been relying on the spot market to fall.

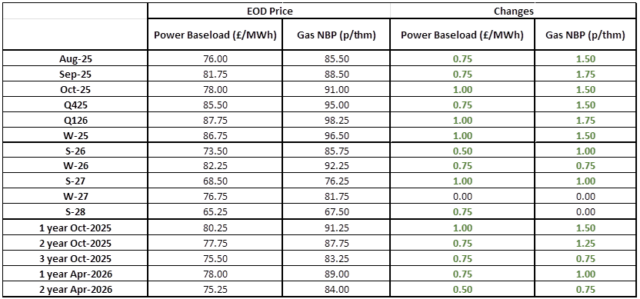

| Gas: Gas prices strengthened at the conclusion of last week. In the prompt, UK domestic demand was 12mcm above seasonal average, supported by the lack of renewable generation. Curve prices rose on the forecasts of a respectively low renewable output, creating further demand for gas-fired output. Power: Power prices continued to rise at the end of last week. In the prompt, a rise in wind forecasts showed an expected output of 7.4GWs/day for today, with an average of 5.9GWs/day over the week. Solar is expected to generate above average at 3.4GWs/day over the week. Curve prices tracked the gains in the gas and oil markets. Oil: The September Brent crude future rebounded back to $70.36/barrel at the end of last week. The IEA made comments believing that the market was tighter than it appeared. The US is discussing further sanctions on Russia, further supporting prices. A decision is to be made later today. Carbon (EU ETS): The ICE Dec-25 fell slightly to €70.55/t on Friday. Opening at €70.05/t this morning, the contract is currently trading at €70.46/t. Carbon (UKAs): The ICE Dec-25 rose to £47.51/t at the end of trading last week. The contract opened at £47.13/t and is currently trading at £47.29/t, down from last weeks close. |

#gas #electricity #businessutilities #businessgas #businesselectricity