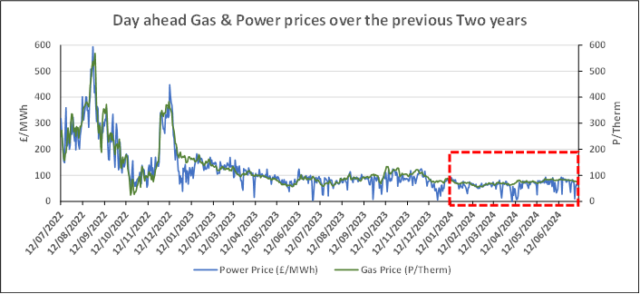

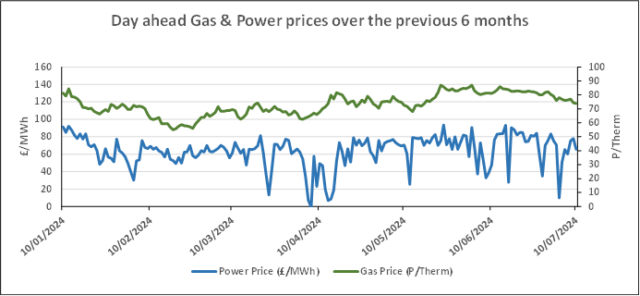

Wholesale Gas and Electricity prices were broadly stable on Thursday following the significant reductions from the early part of the week. As previously mentioned we believe now is a good time to lock in contracts expiring through to the end of September.

At a retail level, credit and sector dependant, we are seeing Gas prices at just over 4p/kWh and Electricity prices marginally below 20p/kWh. Standing Charges continue to rise.

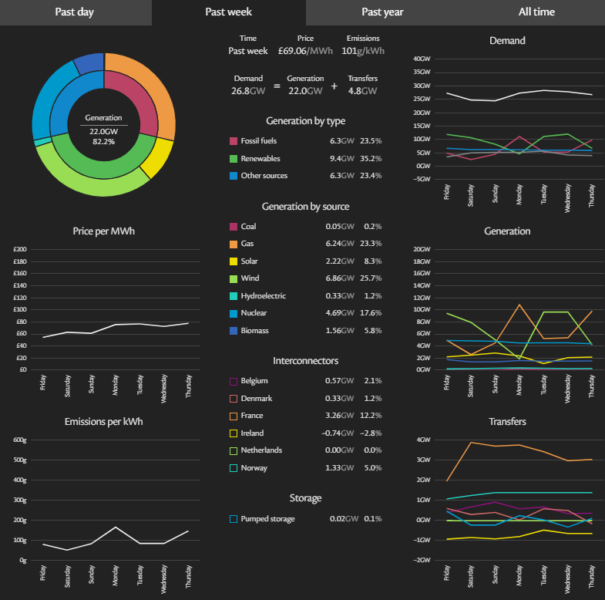

On the generation front, the price at 69.06/MWh for last week was higher than the previous week due to fossil fuels making up 23.5% of total generation, having been below 20% last week. Renewables at 35% was lower than one would have hoped, but given the lower prices of wholesale Gas this did not have as marked an effect as in previous weeks.

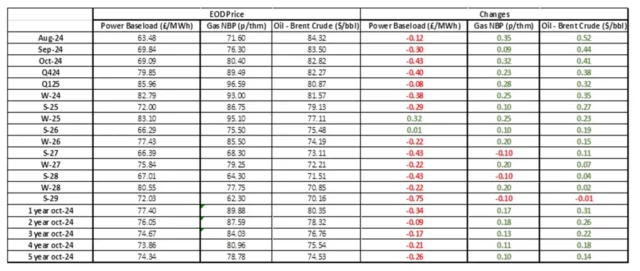

| Gas: Gas prices rose yesterday following an increase in demand for the prompt, due to the cooler weather. Demand for gas-fired power rose as wind generation forecasts fell 20%. Power: Power prices continued to be driven by the wider energy complex. Wind is forecasted to generate 5.6GWs for the remainder of the week, supporting gas for power generation. Oil: Oil prices continued to prove volatile yesterday. US CPI data indicated cooling inflation, keeping trader confidence that the Federal Reserve would cut interest rates in September, thus increasing demand. UK GDP rose by 0.4% in May, after no growth in April, further supporting increasing demand for oil. Carbon (EU ETS): The ICE Dec-24 found some support and rose to €68.37/t yesterday. The contract is currently trading slightly upwards at €68.56/t this morning. Carbon (UKAs): The ICE Dec-24 continues its bearish run and settled at £41.29/t yesterday. The contract has not yet traded at the time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity