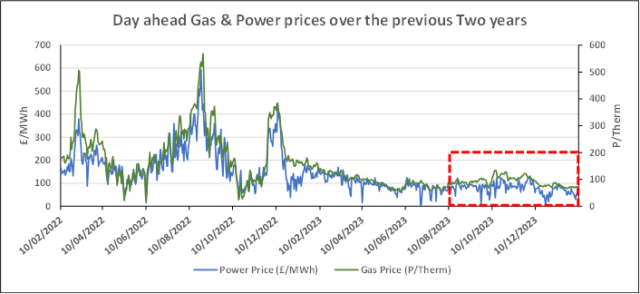

On Friday prices continued to drop for both wholesale gas and electricity.

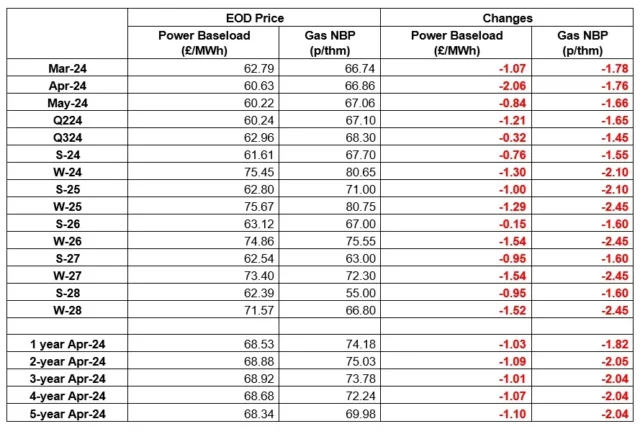

Of note is that Winter ’24 is now at 80.65p/thm and Winter ’25 is at 80.75p/thm. Less than 2 weeks ago we were celebrating them dropping through 90p/thm. The Winter ’24 and Winter ’25 prices are still around 20% above spot prices and, as previously advised, we do expect this gap to shorten during the late Spring and Summer.

It is therefore not advisable to enter into contracts beyond the end of the Summer curve for 2024 at present.

| Gas: An increase in temperature forecasts to 1-3℃ above seasonal norm, combined with an increase in forecast wind generation from 9.7GW to 13.7GW weighed heavy on the prompt at the end of last week with the front month contract seeing a 6-month low. Gas demand is also nominated 61.6mcm below seasonal expectation. Power: Power contracts fell again on Friday as losses to NBP contracts applied pressure. Bearish weather fundamentals added further constraint. (For our traders price outlook, as of Fridays close, please see the table below.) Oil: Oil prices saw large gains throughout the last week, the ongoing fighting in the Middle East has ensured a substantial risk premium is applied to the market. Elsewhere, the Chinese economy had another month of deflation in January where the CPI fell by 0.5% . Carbon (EU ETS): The ICE Dec-24 contract closed at €58.79/t at the end of last week. The contract is currently trading down at €58.10/t. Carbon (UKAs): The ICE Dec-24 gained slightly on Friday, closing at £35.22/t. Opening lower this morning, the contract is now trading at £35.42/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity