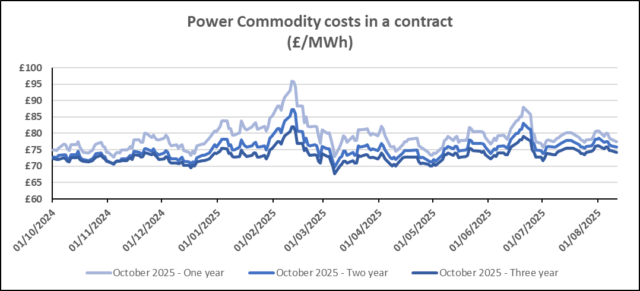

On Friday, wholesale gas and electricity prices dropped, with gas seeing the most significant decrease. While this is a positive development, optimism is tempered by ongoing geopolitical concerns, including Trump’s meeting with Putin and unfolding events in the Middle East.

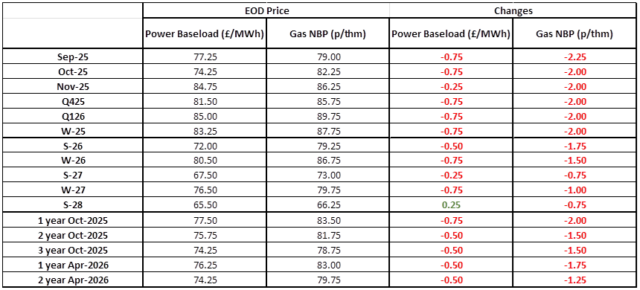

| Gas: Gas prices softened at the end of last week. Above average forecasted renewables for over the weekend saw prices fall in the prompt. As of 7 August, UK gas storage was 34% full, slowly increasing and reducing the risk premiums on the curve contracts. This may potentially be emphasised this week as forecasts expect the system to close 12.3mcm long on average per day this week. Power: Power prices continued to weaken at the conclusion of last week. Power prices continued to shadow the gas market. However, forecasted wind generation has been revised upwards to average 6.6GWs/day, despite it still be lower than average for this time of year. Solar generation is expected to perform well above average, limiting the demand for fuel-fired generation. Oil: Oil prices traded slightly bullish last Friday, settling almost flatly on the previous day but had a weekly loss of 5%. The US and Russia are due to hold a summit early this week to discuss ending the war in Ukraine and removing sanctions on Russian oil and any purchasers of the commodity. Carbon (EU ETS): The ICE Dec-25 rose to €73.21/t on Friday. The contract opened at €72.74/t this morning and is currently trading at €72.99/t. Carbon (UKAs): The ICE Dec-25 settled upwards at £51.86/t at the end of last week. The contract opened at £51.40/t today and is continues to trade that level at the time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity