Wholesale gas and electricity prices dropped at the end of last week, which was welcomed after Thursday’s sharp rises. So far in 2025, wholesale prices have dropped just over 20%, but given the activity in the Middle East over the weekend, we expect further instability especially if Iran blocks the Strait of Hormuz.

While that action has limited effect on UK gas supplies, it does put pressure on the global LNG market and anything that gives traders an excuse to hike prices, they jump at.

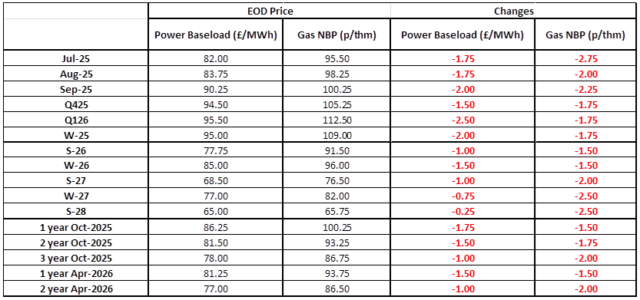

| Gas: Gas prices fell at the close of last week as the market corrected itself after the previous day’s gains. Prompt prices fell as British demand was below average at 127mcm/day, whilst forecasts of strong wind generation for this upcoming week limited demand for gas further. Power: Power prices softened at the conclusion of last week, tracking the wider energy complex and reverting the gains made from Thursday. In the prompt, forecasts expect above average wind and solar generation over the next week, limiting demand for alternative fuel fired methods. Curve prices were influenced by the softening of the carbon market. Oil: August Brent Crude futures fell to $77.01/barrel at the end of last week, reversing the gains made from the previous day. However, prices peaked at $80.32/barrel in the last session as the US escalated the conflict in the Middle East by bombing Iran over the weekend but has since softened back down to $77.18/barrel at the time of writing. Carbon (EU ETS): The ICE Dec-25 rose to €72.97/t last Friday. The contract opened at €72.57/t this morning and is currently trading at €73.00/t. Carbon (UKAs): The ICE Dec-25 fell to £51.00/t at the end of last week. The contract opened this morning trading at £50.90/t and is currently trading at £50.76/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity