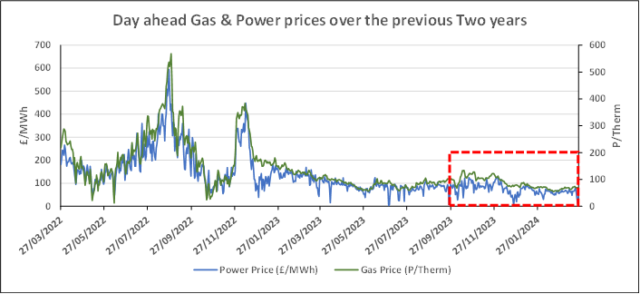

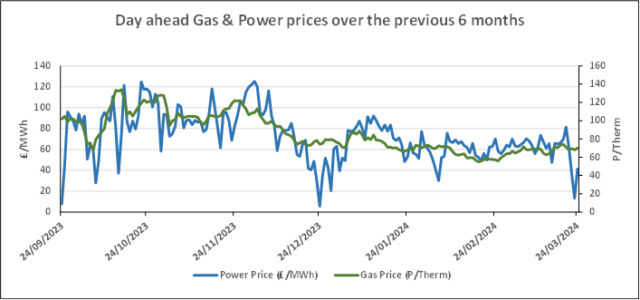

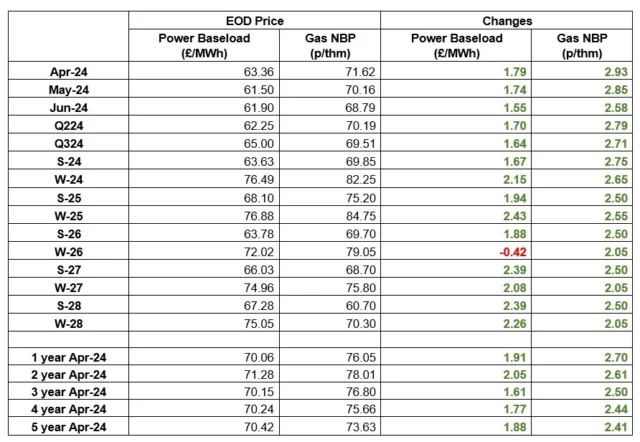

Wholesale Gas and Electricity prices rose on Friday due to trader driven activity in the main, as the market fundamentals remain strongly supportive of price drops.

The challenge at the moment is that new supply is coming on stream in the next 18 months and the suppliers are keen to maximise the prices they get for the gas coming out of the ground.

The increases are not significant but are concerning, and we will review our position later this week.

| Gas: Gas prices rose last Friday. Low LNG send out and lower import levels increased near-curve prices. An increased forecast in day-head demand helped boost near-curve prices further. The UK expects three LNG tankers by the end of March, which is three less than the average between 2018 and 2023. Power: Power prices rose at the conclusion of last week following gains in the wider energy complex, namely gas and carbon. Nuclear generation throughout March has averaged 3.6GWs, 1.4GWs less than the four-year average for 2019 to 2023. Oil: Prices traded flat at the close of last Friday. The week’s sentiment was driven by the delay in US interest rate cuts, and continued pressure for a ceasefire between Israel and Hamas. The $USD continued to increase in value against a basket of currencies, leading to less demand for oil. Carbon (EU ETS): The ICE Dec-24 closed upwards to €61.51/t in Friday’s session. The contract is trading at €63.76/t at the time of writing. Carbon (UKAs): The ICE Dec-24 rebounded from the previous sessions losses to settle at £37.53/t on Friday. Opening at £37.9/t, the contract is showing strength and trading at £38.83/t at the time of writing. |

#gas #electricity #businessutilities #businessgas #businesselectricity