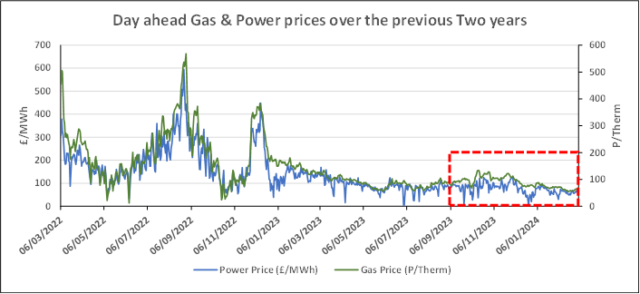

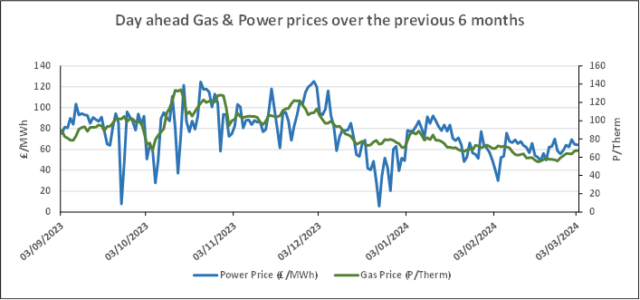

There is continued volatility in the wholesale gas and electricity markets, driven, we believe, by traders closing out inequitable positions contracted before the winter.

The market fundamentals of high stocks, warm weather and secure future supplies remain. We believe that these will drive prices lower in the coming months and years.

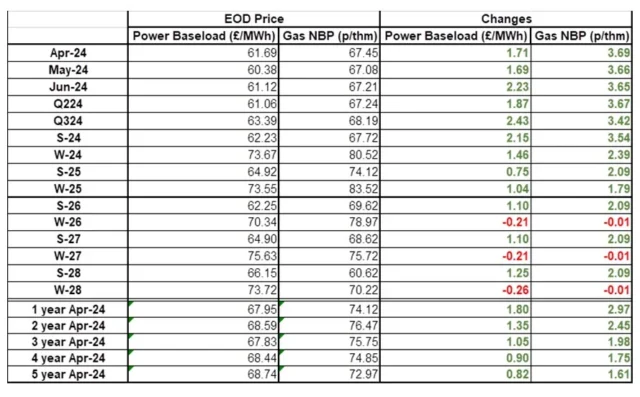

| Gas: Gas prices closed higher than the previous session yesterday. Despite this, the grid was still over supplied by 6.6mcm, with fundamentals remaining bearish. As of 3 March, British gas storage sits at 1,331mcm, 65mcm was withdrawn over the weekend past. Power: Power contracts gained yesterday supported by the rise in NBP pricing. Gas fired power demand in February was down 1.9GW on the previous 4-year average, with lower overall power demand and increased French imports playing their part. Oil: Yesterday’s session proved volatile, with the market waiting on a host of economic announcements due this week. OPEC+ announced that they will extend their supply cuts into Q2 24, and this combined with a weakening US dollar helped add a bullish sentiment. Carbon (EU ETS): The ICE Dec-24 settled at €57.03/t. This morning the contract has traded well with the current price €59.44/t. Carbon (UKAs): The ICE Dec-24 closed at £34.63/t. The contract has opened bullish this morning, currently trading at £35.89/t. |

#gas #electricity #businessutilities #businessgas #businesselectricity