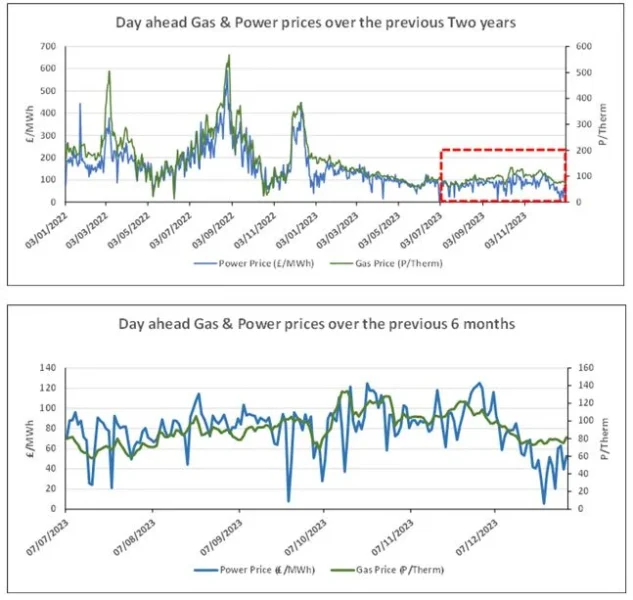

I’m pleased to advise that prices did continue to drop at the end of 2023. The key Gas W24 number is now below 100p/thm, and we expect the reductions to continue.

| Gas: Gas prices fell last Friday. A combination of high winds and the expectation of several LNG cargoes arriving in the UK has kept supplies healthy and demand for gas-fired generation low. The lack of trading over the Christmas period also provided some bearish sentiment to the market. Power: Power prices fell alongside the gas market. Daily average wind generation was revised to 11.3GWs, with temperatures remaining mild. A full capacity outage of 660MWs at EDF’s Heysham 2 nuclear reactor has been offset by the return of Heysham 1, 610MWs, after a planned refuelling outage. Carbon (EU ETS): The ICE Dec-24 rose to €80.37/t at the end of the year. Opening at €80.68/t this morning, the contract is currently trading softer at €77.33/t. Carbon (UKAs): The ICE Dec-24 closed the year at £46.00/t. The contract is currently trading slightly bearish at a flat £45.10/t. |