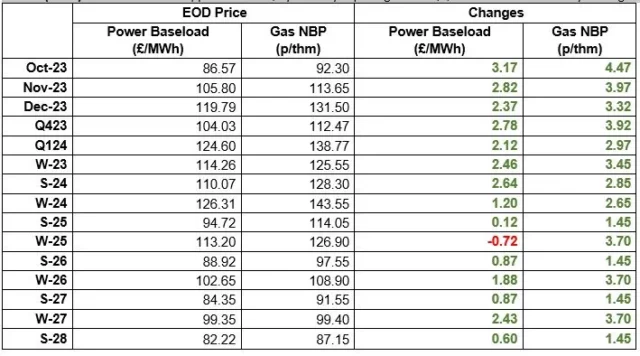

Prices continued their recent see-sawing on Wednesday with rises across the board this time. Again though gas outstripped electricity on the increases. This continues to grow the gap between the 2 commodities where pre Ukraine movements mirrored each other.

| Gas: Gas prices strengthened yesterday due to the combination of Norwegian pipeline maintenance requiring an extension, cancelled LNG imports at Freeport and additional maintenance needed on the BBL pipeline. Price gains were limited in the prompt as Wind generation is expected to create 10GWs/day next week, 20% above average. Power: Power prices shadowed the Gas market yesterday. Wind generation has created 3.2GW/day this week, below the 2018-2022 average of 3.4GWs/day. Crude: Oil prices were volatile yesterday as supply issues from OPEC+ and inflation concerns impacted the market. The IEA continued to raise concerns of a supply deficit towards the end of the year. Global inventories fell to a 13-month low in August. Carbon (EU ETS): The ICE Dec-23 closed at €83.01/t yesterday. Opening higher today at €83.43/t, the contract is trading at €82.81/t at time of writing. Carbon (UKAs): The ICE Dec-23 dropped to £39.03/t yesterday. Opening at £39.2/t, the contract is currently trading at £38.85/t. |